WHAT IS THE VALUE

By Duncan

I like to read about finance, money, stocks, and interest rates. I am also very interested in the housing market. You know, what did the house across the street sell for last week?

I was hired by a mortgage company in the early seventies. After serving in the United States Air Force, I was starting my life over. I know that’s a little melodramatic, but I faced the daunting task of finding a job. I assume this is common. Drop the drama, Duncan.

I entered the man's office and sat on the edge of my seat. I was told what the job was all about. I was going to be a BANKER. Would I get the corner office with the windows overlooking the beautiful landscaping?

No, I was hired as a sales grunt who would pound the streets looking for business. My job was to call real estate offices and beg Realtors to give me the ability to lend money to their buyers/customers. Back in the early 1970s, Realtors worked in an office. They were given a desk and a phone.

My job was to approach the copy machine in our office and make one hundred copies of my rate sheet for our 30-year fixed-rate mortgage loans. Then, I would drive to a Realtor’s office, meet and greet, and provide them with my rates for my FHA, VA, and Conventional home loans.

Of course, it didn’t hurt if you got to know the Realtors on a personal level. I was as green as the grass on a spring day after it rained. I was given a beeper and two charge cards. One charge card is for gas, and the other is for entertainment.

The idea was to take a Realtor to lunch occasionally, get to know them, and tell my story of how I could make the Realtor money by financing and closing their loans faster than the other guys.

The average female real estate broker in the early 1970’s

Of course, the Realtor wants to get paid their commission as quickly as possible. If, for some reason, we didn’t or couldn’t make the loan (turn the loan down), that created a big problem.

“You told me you could make my customers a loan! Your company is full of it!”

The odds of turning a loan down were remote. FHA and VA were 95% of the loans my company made. If FHA or VA said no, we couldn’t insure the loan against default (Federal Housing Administration or Veteran Administration), and my company would have no investor to sell a low-down payment loan. That news always travels quickly in the office to the other Realtors. I would be branded as not being able to get the job done.

Thankfully, it didn’t happen that often. The Federal Government wanted as many people as possible to own a home, and the FHA was pressured to insure as many loans as possible.

During the 1940s-1960s, home ownership went from 43.6% to 61.9%. In the early 1970s, home ownership of Americans rose to 64.5%. The Federal Government slapped themselves on the back and enjoyed a cocktail. Buyers were happy, real estate brokers were delighted, and I was pleased; I made more money than I ever expected.

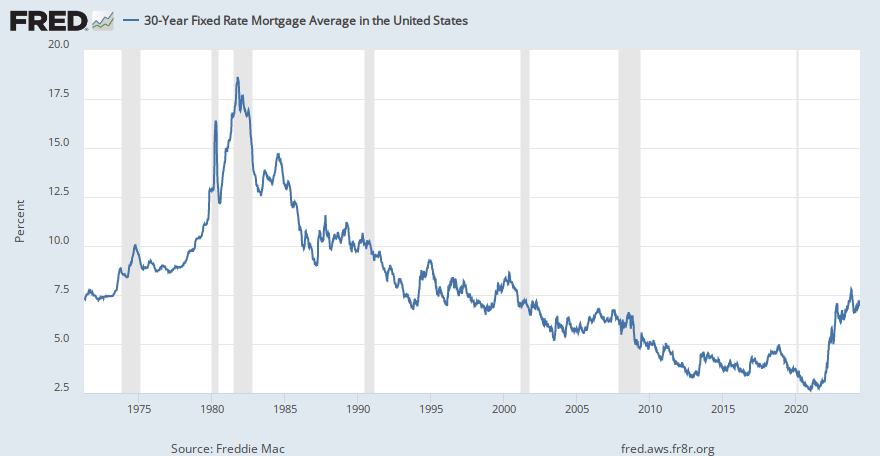

It was a win-win game for everyone. Interest rates for home loans in the early 1970s held steady in the low to mid 7% range.

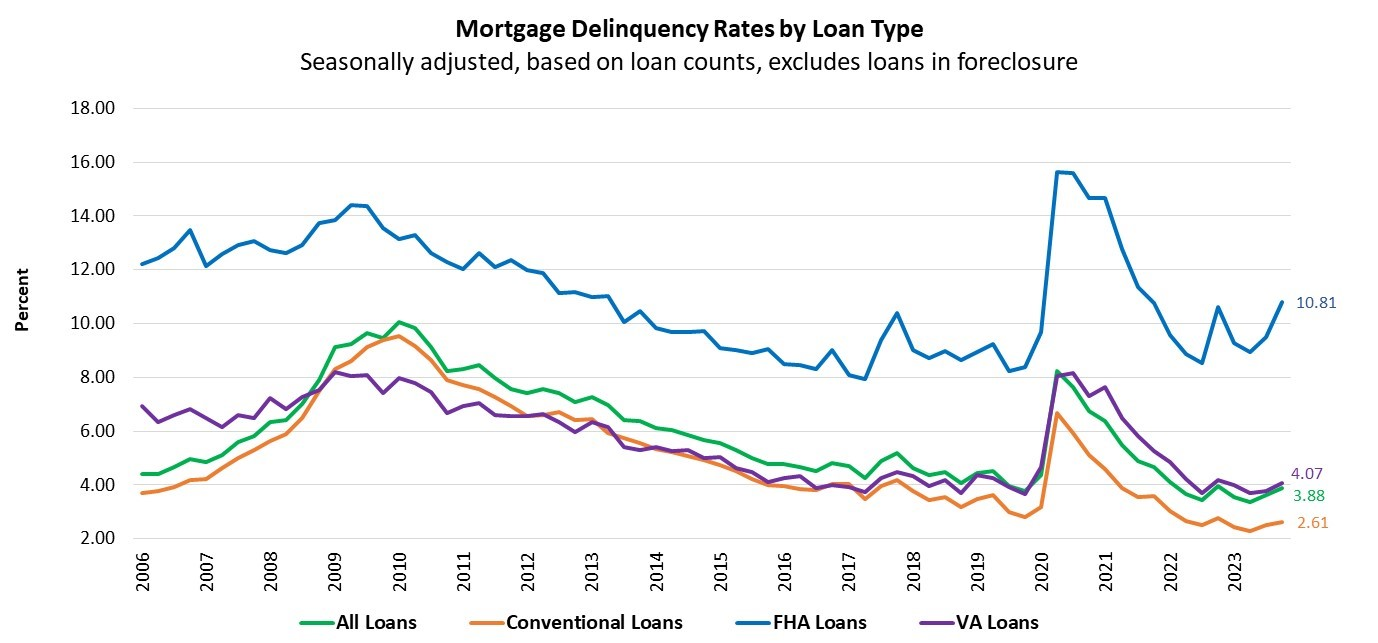

However, the relaxed underwriting criteria handed down from “On High” came with a cost: delinquency rates. People who should not have been given a loan defaulted on their home loans.

The default rate was analyzed by month. How many are behind their mortgage payments by one, two, three, or more months? At six months, lenders foreclose and take the house. We notify FHA and expect them to pony up our money, and we, as lenders, hand the home to FHA. It’s now FHAs responsibility to sell a repossessed house, or in simple terms, it’s called a REPO.

The federal government acts as a sales agent. Yes, default rates increased.

While I enjoyed the early 1970s in the mortgage business, I was able to meet and get to know Realtors personally. I made some very good friends in the early 1970s. However, it took me a while to realize another number. This number is very important to mortgage loan professionals.

It goes like this: 80% of the sales in a real estate office are sold by 20% of the Realtors, and 20% of the sales are sold by the remaining 80% of the sales staff. I was making a big mistake; I was taking the 80% to lunch and could never figure out why the busiest Realtors didn’t have time for me or lunch.

The average male real estate broker in the early 1970s

In today's housing market, it’s a whole new ballgame. I’m retired from the home mortgage business and have no interest in returning to the game. Housing prices are up, up, up. And why is that?

Oh, there is always the supply-and-demand rationalization. When interest rates were 3.5% for years, many homeowners refinanced their higher mortgage rates to low single-digit rates. (It’s hard to believe everyone switched to a 3.5% rate, but maybe they did.)

My experience was when I returned from Florida in mid-2019. The explosion of home prices was starting. The home I own today had five offers. And I’m told it was on the market for five days.

|

| SUSAN TIBBS - TUCKER - 317-507-8490 |

I gave up the inspection and an appraisal. I wanted the home.

So, WHAT IS THE VALUE of a home? Who decides what the house is worth? In today's market, it ain’t the appraiser who establishes value anymore. It works the same way it’s always worked. The VALUE of a house is established when a willing seller and a willing buyer agree on a price.

(First row, far left) - Lucy Duncan - My Mom

1989 - Christmas - Staff at the Metropolitan Indianapolis Board of Realtors